Any savvy lessee can tell you that the key to getting a good lease is “knowledge”. If you don’t know how to estimate payments, you run the risk of being fleeced by your salesperson. The only way to prevent this is to determine what a “realistic” payment is and try to work with your salesperson to achieve that. Realistic payment estimates are essential because no dealer will work with you unless they are able to make some money out of each transaction. Like us, they got bills to pay too. Below, your will see a few lease calculation examples that should help you with your negotiations.

Calculating Your Payment – Inception fees due at signing

The quickest way to estimate lease payments is to assume you will be paying your inception fees upfront. This way, your calculations remain simple and quick. All you need are the basics: MSRP, Sale Price, Term (in months), Residual Value and Money Factor. If you want to take advantage of the RWG rating, you will need to know your mileage allowance as well. Check out the example below:

2012 ACURA TL BASE

36 month | 15k miles | residual 61% | .00170 base money factor

MSRP – $36,490

Sale Price – $32,567 (TrueCar price minus $1000 rebate)

Monthly – $380+ tax

RWG Rating – 93.9

The assumption is that you will pay your inception fees upfront and keep it separate from your loan. Since the drive-off (inception) fees fluctuate depending on the cost of the vehicle, I generally assume it’s approximately $1500-$2000. Inception fees normally consist of the following: Your first month payment, Bank Fees, Dealer Fees, County/City fees, DMV registration and sales taxes associated to any rebates you are getting. In some states, you may have to include the sales tax for a portion of your lease depreciation or 100% for your vehicle’s value. For most states, sales taxes are calculated as an “use tax”, which is applied to your payment on a monthly basis.

Based on my location, my inception fees would amount to approximately $1335. Here’s how I estimated that:

DMV $315 (CA DMV Registration Calculator)

Bank Fee $595 (List of Bank Fees)

Dealer Doc Fee $45 (Capped in California, other states are uncapped so could be in the hundreds).

First Month Payment $380

Total Estimated $1335.

This number is actually low because there are extras fees associated with your DMV registration. In addition, cities will sometimes charge extra fees here and there as well. If the dealer does electronic filing of your registration, there will be a cost associated with that too. If that wasn’t enough, you also have to pay taxes on any rebates and any advertising fees that certain dealers charge (Think MACO and Training for BMWs). When it’s all said and done, expect to pay AT LEAST $1335. To be on the safe side, I like to estimate my inception fees to be in the $1500 range and if you pay advertising fees, it’s more like $2000. The best way to know what you are paying for is to have your dealer itemize these fees so you know exactly where your money is going.

Once you have determined what to expect (in this case, you are looking at a $1500 drive-off with a $380 monthly payment +tax) you will know what to tell your dealer when they ask you how much you can “afford” per month and how much you plan to “put down”.

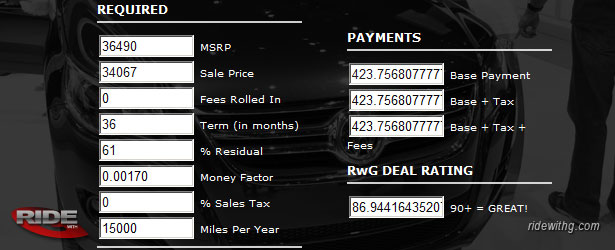

Calculating Your Payment – $0 Drive-Off

To get an idea as to what you would be paying per month on a $0 drive-off deal, you simply add-on the drive-off to your sale price. In this case, we know the sale price minus the rebate on the 2012 TL is $32567 and we estimated our drive-off to be about $1500. This comes up to a total of $34067 for your sale price (which we generally refer to as cap cost). In order to figure out the monthly payments, just plug the total into the sale price Fees to Roll In (thanks for the correction BD) field of the calculator and hit “calculate”. If you have to pay all your sales tax upfront, add that in there as well.

2012 ACURA TL BASE

36 month | 15k miles | residual 61% | .00170 base money factor

MSRP – $36,490

Sale Price – $32,567 (TrueCar price minus $1000 rebate)

Fees Rolled In – $1500 (Estimated inception fees)

Monthly – $424+ tax

RWG Rating – 93.5

One thing to note here is that this is a simplified approach, so your dealer’s numbers will vary slightly (usually a little higher). However, I think that you should be within reasonable dollar amount so it shouldn’t be that big of a deal.

It is more advantageous to do a $0 drive-off lease when the money factor is low. Please note that the $0 drive-off leases do take a very small hit on my RWG rating system (about 0.4 pts) and that is due to the fact that you are paying interest and taxes on items such as your DMV registration, bank fees, dealer fees, and so on. But in the grand scheme of things, those costs shouldn’t be too significant if your money factor is low.

RWG Rating System

The rating system I use is fairly straight forward. Anything above a 90 rating is considered a good lease. Ratings higher than 100 are exceptional. Ratings lower than 85 should probably not be considered. Personally, I would not recommend leasing anything below a 90 rating if getting more car for your money is a top priority. If you are willing to pay a little extra to get what you want, I wouldn’t go below 85. Please note that the rating does not take into consideration sales taxes and it also assumes you will pay your inception fees up front.

If you plan to use the rating system to compare $0 drive-off deals, make sure to do that for all cars to ensure a fair comparison. I would recommend adding $1500 to the sale price for all vehicles in the comparison to compensate for the usual drive-off costs.

How to Identify Good Deals

There isn’t a fancy way to figure out what makes a lease a good one. The best way to get a “DEAL” is to make sure at least TWO of the THREE main components of a lease are attractive. By components, I mean the following:

Residual Value. The first thing I look for is a HIGH Residual Value. I do not typically buy my cars at lease-end so leasing a car with a low residual value doesn’t make any sense. Because of that, I like to go for models that have residual values in the high-50% or low-60% on 36-month terms. I find 36-month terms to be optimal in terms of payments and wear-n-tear. 24-month are great, but may feel a tad short, while 48-month leases are too long and add too many unexpected expenses.

Money Factor. You want to keep this low so you don’t get charged too much interest on the loan. I usually shoot for leases with the “four zeros”, the ones that fall below 0.00100 or 2.4%. You can calculate the interest rate by multiplying the money factor by 2400.

Sale Price. An aggressive sale price is also a great way to keep your payments low. As you know, the size of your lease loan is determined by the difference between your sale price and residual value. If the gap between your sale price and residual value is low, the size of your loan will be smaller. This will also help keep the finance charge (money factor/interest) minimal, thus keeping your payments lower. Sale prices that are close to 10% off MSRP are probably the best. Any percentage above that is just icing on the cake. A good deal hunter would generally look for a vehicle that sells for a big discount (plus rebates and incentives), high residual value and low money factor. This combination typically yields the lowest monthly payments and gives us the most bang for the buck.

What’s a good example of a good deal? For the month of July 2011, the 2011 Infiniti G37 Journey Sedan looks very attractive. It boasts one of the higher residual values for 2011 models (58% @ 15k miles per year over 36-months) and has an easy-on-the-pocketbook 0.00058 money factor that breaks down to a low interest rate of 1.4%. The average sale price for this sedan in the Southern California region is 12% off MSRP and as of July 2011, there’s $1000 loyalty cash and $1000 dealer cash that’s available until August 1st, 2011. This certainly isn’t the only car that’s considered a good deal, but it’s one of them.

Here’s are some helpful links to get you started on how to estimate your own lease payments:

- RWG Lease Calculator

- Captive Bank Fees

- Lease Rates

- Local Sale Prices (TrueCar)

- Available Incentives (Edmunds)

Now go find yourself a good deal!

G,

Have you found that there are any particular months of the year that are “sweet spots” for leasing? The time when “deals”, residual value and MFs all merge to produce the best monthly rate for a given vehicle? Summer-fall when new MYs are around & residuals are high, or winter with year-end deals, or spring with deals and good MFs?

Thanks.

@Joe. In the past, it’s been the 2nd half of the year. However, this year has been weird cuz of the Tsunami, so leases started to get more expensive after March/April. On a normal year however, I find May-Aug to be pretty good. Holiday season is also quite good on year-end models. Jan/Feb typically not so good.

Do you have info on Ford Explorer Limiteds?

Can I get a copy of your latest excel model. I would like to compare so lease deals.

thanks,

Rob

@rob. I normally would, but last time i made the spreadsheet available, people started rebranding it and calling it their own and using it on their websites. I know it’s a bit more inconvenient, but please use the web version found here: http://www.ridewithg.com/calculator/index.html

Hi G. The reference to the Infinity money factor above at 0.0058 is probably 0.00058?

Thanks for catching that Ali! That extra “0” makes a world of a difference. Haahaa.

OK, no problem, I understand. I just wanted to compare leases and it looks like you have a good model. I was looking at the calculator and it looks like you use 48 mo lease in your rating system. Why use 48 and not 36 mo. Also, you rating weightings don’t at to 100%. Any readon for that. Your site is great and very informative. Thanks!

Rob

@rob. The 48mo lease is a good base term (altho 36mo term is optimal). MB offers very reasonable 48mo leases, which is why 48 was chosen over 36. Had I used 36 months, there wouldn’t be an effective way to measure 48mo leases because they would have been overated.

I chose 95% instead of 100% because it provided a greater balance in the rating system. Giving that extra 5% to either the term, payments or the mileage overvalue those categories. I wanted to get as close to the 100 rating without exceeding it, unless the deal was phenomenal.

The rating system will eventually need to be adjust as pricing trends begin to change. For now it is still very effective, so no changes are necessary. Hope that answers your questions.

G, thanks for the repsonse. That answers my questions. Good stuff.

Thanks again!

Rob

Is there any advantage in a 1 pay lease?

Thanks

@joe. Yes. Bank usually give you a discounted MF, so you pay less in interest. I have mixed feeling about this method though.

Hi G,

When you say 90 is a good lease is that factoring in MSD’s.

Thanks

Yes. MSDs you get back at lease end, so you aren’t losing that money. When MF is high and you are given the choice to use MSDs, do it.

Im running numbers on an M3 and C63 with your calculator and Im wondering how the calculation actually works – im getting the car for 1000$ over invoice which is usually considered a good deal – your calculator rates it 57. What gives?

@balte. Lease rating is based on more than just the sale price. The rating evaluates the MF, Residual, Sale price and how many miles you get in your deal. M3 and C63 are not good leases. I’ve only seen a M3 convertible with a good lease offer in the 4 years I’ve been running this website and that was last year during the fall/winter. Just looking at the MF you pretty much know you are paying a premium to lease one of these cars. Leasing is more complex than buying because there are more factors to worry about. With buying, all you worry about is the sale price and at what interest rate you borrow money from. Leasing considers how much money you borrow, which varies depending on the residual and the agreed upon sale price. Not a straight forward. hope this makes sense.

Opinion requested.

I have an offer to lease a TSX special edition 36 month for $269/ mo +tax with $1700 down

I know the msrp is $33905 and the net cap is $28930…

OR 36 month with $0 down for $320 +tax.. Residual value is 59% and mileage allowance is 10k/year. I don’t know MF yet. How can I tell if this is a good lease?

trying to plug into your calculator seems good, BUT I am guessing at a few details.

thanks for any help or feedback

If plugging into calc looks good, the probably not half bad. I do wonder about the 1700 due at signing tho. Seems high in order to get the $320 payment. Plus only 10k a year?

Hi G, Thanks for the very informative and helpful website! My question is regarding a 2013 Civic EX L with Navi. I ran the numbers the on the deal on your calculator, and the disparity is about 44.00 a month from what the dealer quoted. details are as follows:

36 mo lease/12000 m

MSRP 24555

Sales Price 22388

Invoice 22867

Residual 14487.45 59%

Money Factor 0.001150

Ca sales tax 7.5

I was quoted 304 w/o tax and the calculator comes up wit 261. It isnt clear to me how to figure out where this disparity is coming from? Could this be the difference of 1300.00 in inception fees? this is a 0 down, 0 security, 350 drive off, and 35 payment deal. If that is the case I would assume my best bargaining power is with the money factor and sales price? Thanks

Hi Rusty, you hit it right on the nail. Typically, a $0 drive-off lease will require that you pay for all of your fees as part of your monthly payment. When it gets rolled in, you are paying taxes and interested on the inception fees. Negotiating the money factor may not get you anywhere, but I think Honda has in the past discounted the MF on $0 drive-off deals. Not sure of that is still going on right now though. Your best bet is to tackle the sale price, although, I’m not sure how much lower you can go. That’s a really aggressive sale price.

Thanks G!

You are the man! We are in final negotiations and it is good to know that even if they don’t budge from here, this deal is worth it to me. Once again, thanks for your excellent website, and your quick response to my questions.

I’m wondering why in your $0 down example you don’t add anything to the “Fees Rolled In” field, and instead add the inception fees to your sales price. This seems counterintuitive and drastically affects the RwG deal rating. For example, the RwG score jumps to 93.5% in your Acura example if you move the $1,500 in inception fees to the Fees Rolled In field. The increase seems to be caused by the increase in the “percentage off MSRP” that is caused when you exclude inception fees from the sales price.

Moreover, I don’t think it makes sense to have one RwG score for a lease in which the inception fees are paid up front and another for the exact same lease where the fees are rolled into the cap cost. This discrepancy is eliminated if you add those inception fees to the Fees Rolled in Field, where they seem to belong.

Thanks for chiming in. I made the correction in my write-up. Greatly appreciate your valuable feedback!

In the details of your clauclator 3.1b, I noticed a “rent charge”. What is this? Is it negotiable?

Rent charge is basically the MF. How much you pay in interest for the loan. Normally not negotiable.

What States do NOT allow an MSD? I was told N.Y. State does not allow it to be used.

At the moment, I only know NY as well. Haven’t heard from other states.

Look at any lease agreement and you will find that the cap reduction (down payment minus fees) includes your 1 month payment. This is fine except that they use that figure to determine your depreciation. They then take the depreciation and divide by months of your lease term.

My question is:

If your are paying the 1 month payment up front, how can they use that figure as part of the depreciation?